It’s that magical time of year again. Thanksgiving is over. Black Friday has come and gone. Mariah Carey is blasting in retail outlets and Starbucks stores across the country. Once again, I am trying to convince friends and family to watch Home Alone with me. The holiday season is in full swing, but so is another season: Wall Street Next Year Forecasts.

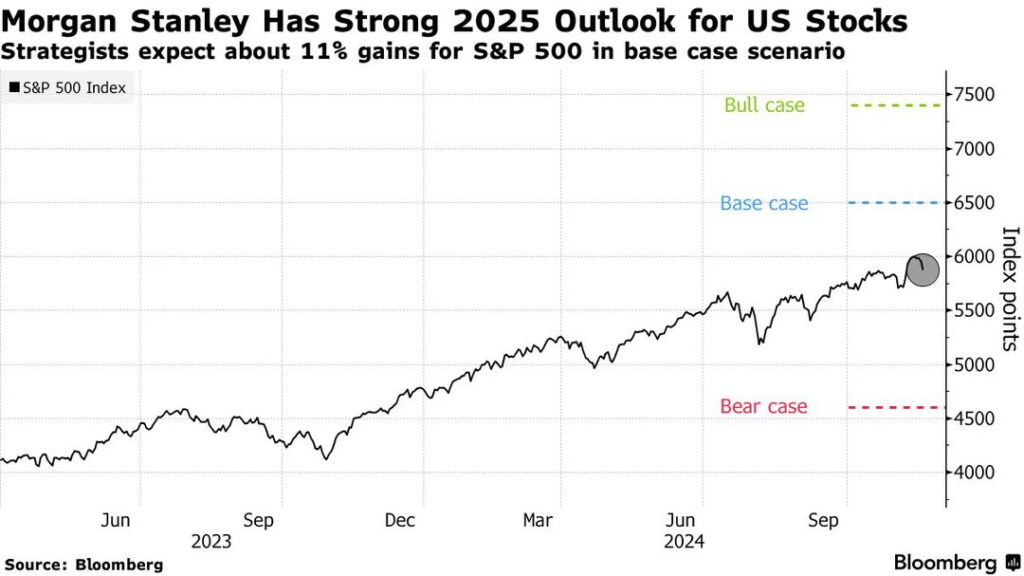

Over the past few weeks, we started getting forecasts from some of Wall Street’s biggest banks and investment managers. According to Bloomberg, “In their worst-case scenario, the S&P would drop 22% to 4,600 points while the most bullish case would see the index surge 26% to 7,400 points.”

Expect Average Returns, But…

The economy and stock market grow, on average, by 2-3% and 10%, respectively. These are generally good approximations based for what to expect. While the stock market average is 10%, it has a volatility of ±20%. That’s a pretty wide range. Again, this is based on historical returns. The stock market usually performs within this wide band, but sometimes it goes way outside. However, our best guess is within ±20% of the 10% average return.

Looking at all these 2025 forecasts from the big banks and investment managers, they come in around the historical average, even though some of them have extreme forecasts.

There is always that one guy being a bear—he’s the most annoying co-worker at every holiday party.

What’s the point of guessing the average?

It’s really easy to say, “I can make that same guess; please pay me a fraction of what one of the market strategists makes.” I get it. However, we can learn a lot through this exercise and develop an expectation of what markets may do and adjust asset allocations.

Strategists develop a base case, form some upper and lower bounds, and then adjust throughout the year—they change forecasts with new data.

The head strategists of Goldman Sachs expect the S&P 500 to finish around 6,500 points next year, which is about 7.5% higher than when I write this. Morgan Stanley’s market strategist came up with a similar number—not a bad year. It’s a little less than average but way less than the mid-20% we have seen in the last two years.

Returns are likely to be lower than in the past two years

What gives? Well, the big tech firms put up some insane profit numbers over the past couple of years, in particular the Mag-7. From a recent OddLots Podcast, Kostin of Goldman Sachs argued:

“those companies had 33% expected — well, not expected because it’s the fourth quarter, but let’s use that as a full year number — earnings growth around 33%. And that compares [to] around 3% for the 493 remaining companies in the S&P 500. That’s 30 percentage points excess growth rate.

And the coming year, the expectations views consensus for a moment is around 18% versus 12%. That’s a six percentage point gap. So from 30 percentage points to six percentage points, and you look into 2026 and that’s going to narrow yet further until around four percentage points. So relative earnings growth is going to be the explanation, in our view, of a narrowing premium return.

And so if I put some numbers around that, very specifically, you had 63 percentage points of outperformance — excess return — of the largest stocks versus the market in 2023. It’s running around 22 percentage points this year. And our forecast next year is probably around seven percentage points. So the largest cap stocks [are] likely to continue to outperform in our view, but by a much, much smaller margin than has been the last couple of years.”

It’s been no secret that the largest companies have carried the index the past couple of years. I often say something like “a handful of stocks carries the entire index” or “a few stocks rule them all,” which is true. However, the past two years have been ridiculous with Nvidia making up like a quarter to one-third of the gains for the S&P 500, at different points. It’s mind-boggling how heavy the AI trade has been.

The insane profitability of the Mag-7 is why they have driven the S&P 500 to record highs. After all, in the long run, the stock market is driven by profits—not vibes.

The S&P 500 Is Carried by a Few

To the extent that you have diversified at all, you have been left behind. The Mag-7 are responsible for all of the gains. If you are a diversified asset manger benchmarked to the S&P 500, you have had a bad time.

If we look at the market-cap weighted S&P 500 and compare it to the equal-weighted S&P 500 (above graph), we can see the performance gap is enormous. Same 500 companies for both lines, but when the biggest make up the biggest portion of returns, it can get very lopsided. Diversification has not been our friend the past two years like it was in 2022.

It’s a big deal that market strategists continue to see the “normalization” of profits in the Mag-7 (specifically the tech sector). Strategists expect for the other 493 companies to close the gap. A less narrow market or broad market rally is generally considered to be healthier—less susceptible to big drawdowns from one sector’s price correction.

While the big tech stocks are still expected to grow earnings, and by a lot, we aren’t expecting them to continue to grow earnings by thirty percent over the other 493 stocks. It’s not sustainable. But we also figured that last year, so who knows?

Predictions Are Hard

I had a college professor say, “Predictions are always wrong, so the trick is to be less wrong than everyone else.” I think this sentiment is generally correct. We can’t predict the future with a high degree of certainty or consistency, so we should expect to be generally wrong.

That doesn’t mean this exercise is useless:

- The analysis concludes that stocks should rise over the next year.

- We should expect the earnings growth of the other 493 companies to carry more of their weight in the S&P 500 than in the past two years

- It also shows that there is a wide range of potential outcomes around that expectation—wider than normal

- Forecasting earnings is more reliable than forecasting valuations. If market valuations are a bit stretched, it’s less likely to get sustained expansions—meaning it will be more about earnings next year

Right now, I know you’re thinking, “If forecasts are hard the average is fairly accurate, we should expect the average and move on, right?” It’s not so simple!

How Common Is the Average?

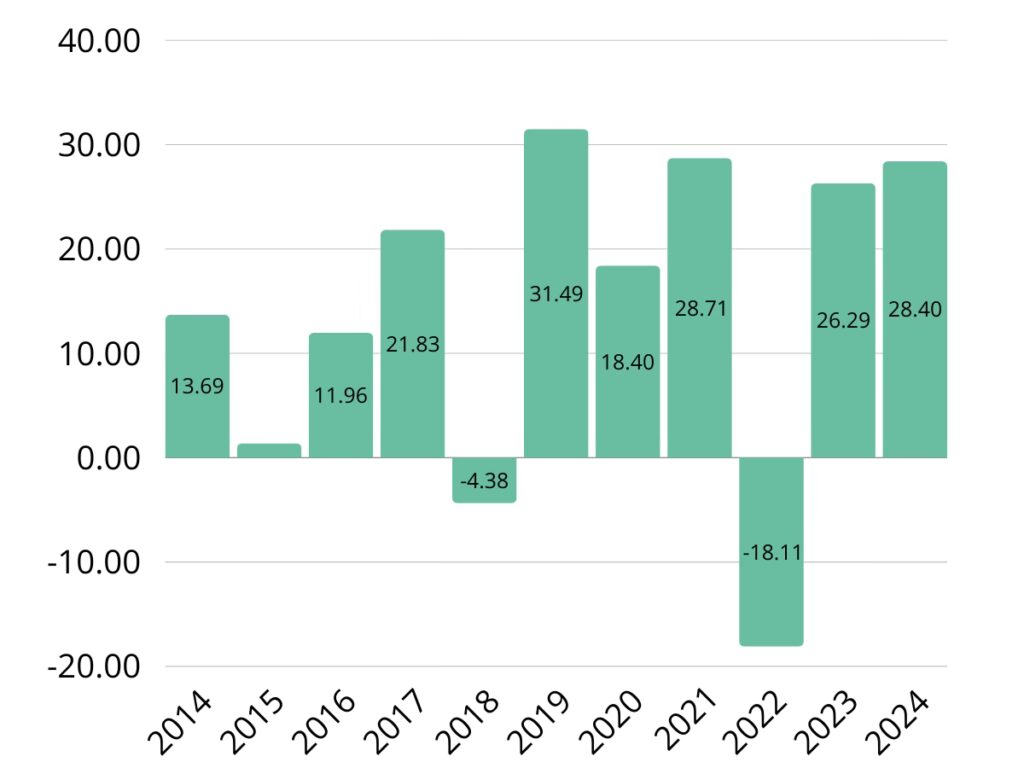

Looking at the graph above, you can count on two fingers how many times the S&P 500 has delivered its historical average return over the past 10 years. However, it performs within that range of roughly ±20% around the average. The “average” return is quite uncommon.

So, what can we take away from Wall Street’s forecasts?

For one, we should expect a wide range of potential outcomes. While the base case suggests a moderate gain, we should expect that market performance could land anywhere.

Second, the era of massive outperformance by a handful of mega-cap stocks may be fading, leading to a more balanced and stable market. Analysts have gotten quite good at predicting earnings—the most reliable driver of returns.

Finally, the current environment—characterized by growing earnings and falling inflation—appears favorable for equities.

TL;DR

Wall Street’s forecasts remind us of the inherent uncertainty of investing but also offer a roadmap for navigating that uncertainty. By understanding the factors driving market expectations and the risks involved, investors can make informed decisions about their portfolios. As the holiday season enters full swing and the new year approaches, it’s a great time to reflect and plan—whether for our holiday celebrations or our finances.