A 529 plan is a savings plan is one of the best ways to save for tuition or college expenses. A 529 offers many tax benefits and designates an individual’s tuition and related education expenses. The two main 529 plans are prepaid tuition and more typical college savings plans.

Prepaid tuition plans allow the account owners to effectively lock in costs today for designated colleges or universities in the future. College savings plans allow account owners to save on a tax-deferred basis and make tax-free withdrawals for tuition and qualified expenses.

Tax Advantages of 529 Plans

The primary tax benefit of a 529 plan is that earnings grow tax-free from both federal and state income taxes. Unlike traditional retirement accounts, contributions made to 529 plans are not federally tax-deductible. However, some states allow for the deduction of income taxes on any contributions made to a state-sponsored 529 plan.

Changes to 529 Plan with Tax Cut and Jobs Act

The Tax Cut and Jobs Act of 2017 expanded the college savings plans to include tuition costs of K-12 schools. The 529 college savings plans allow tax-free withdrawals for tuition, room and board, textbooks, and technological needs for post-secondary education.

With the TCJA, parents can use a maximum of $10,000 per year for tuition. Unlike college expenses, parents cannot use the plan for textbooks, computers, or supplies. Only tuition is eligible for K-12 tax-advantaged withdrawals.

Changes to 529 Plan with the SECURE Act

The Setting Every Community Up for Retirement Act (SECURE Act) allows 529 plans for apprenticeship programs and allowances for student loan repayment. The apprenticeship must be registered and certified with the Secretary of labor to qualify for 529 plan expenses.

Student Loan Repayment

The law allows a lifetime maximum student loan repayment amount of $10,000 per beneficiary. Beneficiaries may pay principal and interest with the 529 plan. However, the beneficiary can not take the student loan interest deduction for that interest amount paid by the 529 plan.

For amounts leftover in the 529, the owner may change the beneficiary to a sibling without tax consequences. The sibling may then use the 529 plan to cover qualifying expenses and w$10,000 in student loan repayment. The $10,000 maximum is per beneficiary and not the plan owner.

Apprenticeships

The SECURE Act now allows the use of 529 plans for apprenticeship programs. For the apprenticeship to qualify for 529 plan expenses, the program must be registered and certified with the Secretary of Labor under section 1 of the National Apprenticeship Act.

Apprenticeship programs provide on-the-job training to prepare workers for a specific career. Many industries offer this form of training, such as healthcare, construction, information technology, logistics, manufacturing, etc. 529 plans will cover fees, textbooks, supplies, equipment, and tools required for the trade.

Who Can Open a 529 College Savings Plan?

So, who can open up a 529 plan for future education expenses? Anybody can own a 529 college savings plan for a qualified family member:

- Yourself

- Son, daughter, stepchild, foster child, adopted child, or descendent

- Son-in-law or daughter-in-law

- Siblings or step-siblings

- Brother-in-law or sister-in-law

- Father-in-law or mother-in-law

- Father or mother or ancestors of either stepmother or stepfather

- Aunt, uncle, or their spouses

- Niece, nephew, or their spouse

- First cousin or their spouse

You can open a 529 college savings plan for kids or adults in which you have any of these relationships. Essentially, you can’t open a 529 for your neighbor or a random stranger. It is also important to note that you may name a different qualified beneficiary without tax consequences if the original beneficiary does not use all of the funds.

How Much Can You Contribute Annually To a 529 Plan?

Retirement accounts have contribution limits. Traditional and Roth IRAs have a limit of $6,000 per year, and 401(k) accounts have an annual limit of $20,500 per year. However, 529 plans are different from other tax-advantaged accounts because the IRS does not set an annual limit on contributions.

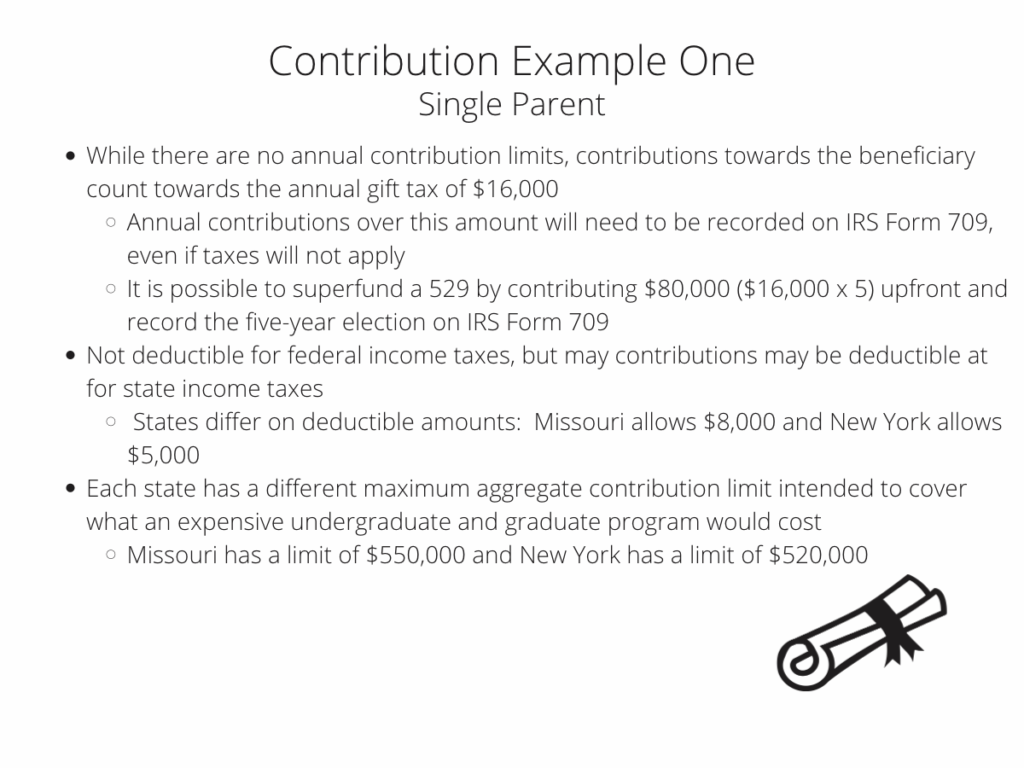

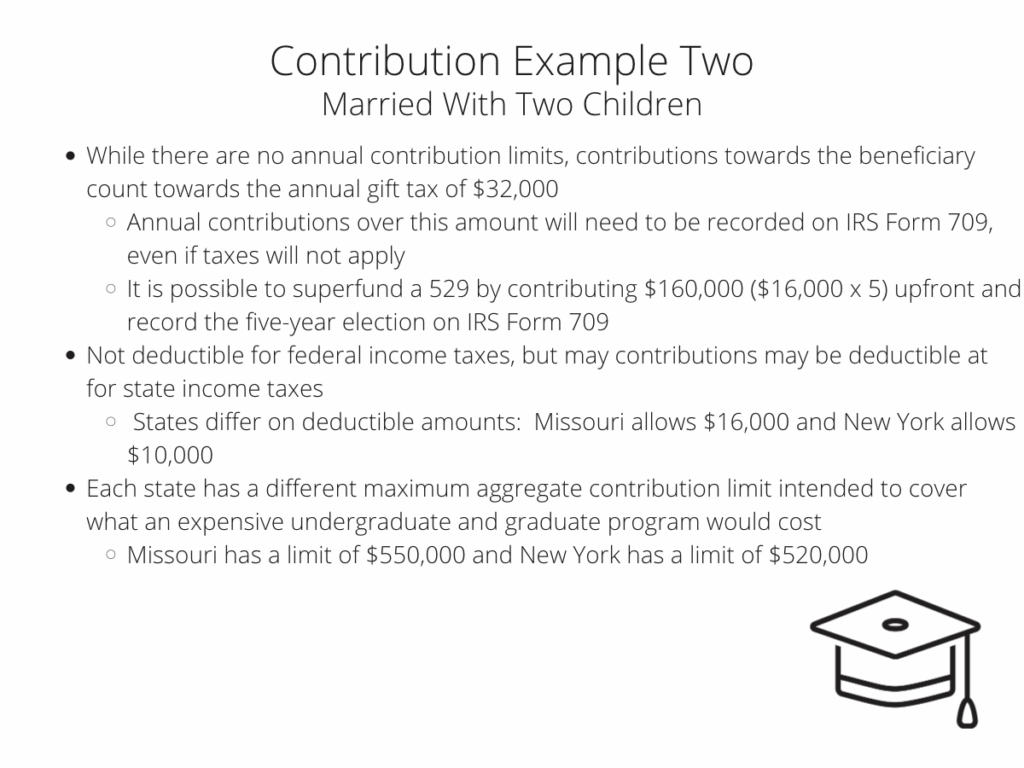

While there is no annual contribution limit, there are a few other rules to consider when making contributions. Saving money for your child in a 529 plan counts as a gift for tax purposes. Gifts are limited to $16,000 per year per individual for 2022. If you are married with two children, you and your spouse can give up to $64,000 per year without going over the limit.

It is possible to “superfund” a 529 plan using a 5-year gift tax average. For 2022, individuals may contribute $80,000 to superfund a 529 and then record the five-year election on IRS Form 709. This strategy comes in handy for parents and grandparents looking to shelter assets for estate planning purposes.

Contribution as a Single Parent

Contributions as a Married Couple

Maximum Contributions to 529 Plans Differ Among States

Also different from 401(k) and IRA plans, 529 college savings plans have aggregate contribution limits. The law states that 529 plans cannot exceed the expected cost of the beneficiary’s college. So, 529 plan limits differ from state to state. Limits range from $235,000 to $550,000:

- Missouri limit of $550,00

- New York limit of $520,000

- Illinois limit of $500,000

- Florida limit of $418,000

- Georiga limit of $235,000

Why You Need to Use Your State’s 529 Plan

As mentioned previously, 529 plans are not federally tax-deductible. However, over 30 states currently offer an income tax credit or deduction when you contribute to the state 529 plan of your residence.

The states set their own rules for 529 deductions, so there is some variance among the rules. For example, state tax deductions for Missouri 529 plans are $8,000 per person and $16,000 for married couples. In contrast, New York offers a $5,000 tax deduction for individual contributions and $10,000 for a married couple.

However, it could still make sense to use a bonus, financial windfall, or pile of cash to superfund a 529 savings plan, even if holders cannot use the tax deduction. The earlier, larger, and more frequent the contributions, the longer the funds can compound for future college expenses.