Inflation seems to be all the rage today with traditional and financial media, and for a good reason. Globally, inflation rates have increased significantly over 2021. Inflation rates are running higher for consumers than in over a generation, and that has many people asking: How does inflation work? Should I be concerned about inflation? What is causing Inflation? How long will inflation last? What can I do to protect myself from inflation?

Key Takeaways

- Inflation Defined

- How Does Inflation Work

- Winners and Losers of Inflation

- Tradeoffs and the Dual Mandate

- How Fast Is Inflation Rising?

- How To Invest With Inflation in Mind

What Is Inflation?

Broadly defined, inflation is the erosion of purchasing power of money. It can be challenging to measure it precisely and notoriously difficult to predict. Economists use a basket of goods to compare prices over long periods to get the best inflation estimate. That basket is kept relatively stable but adjusted for changes in quality or obsolescence. If this sounds complicated, it’s worse than you think.

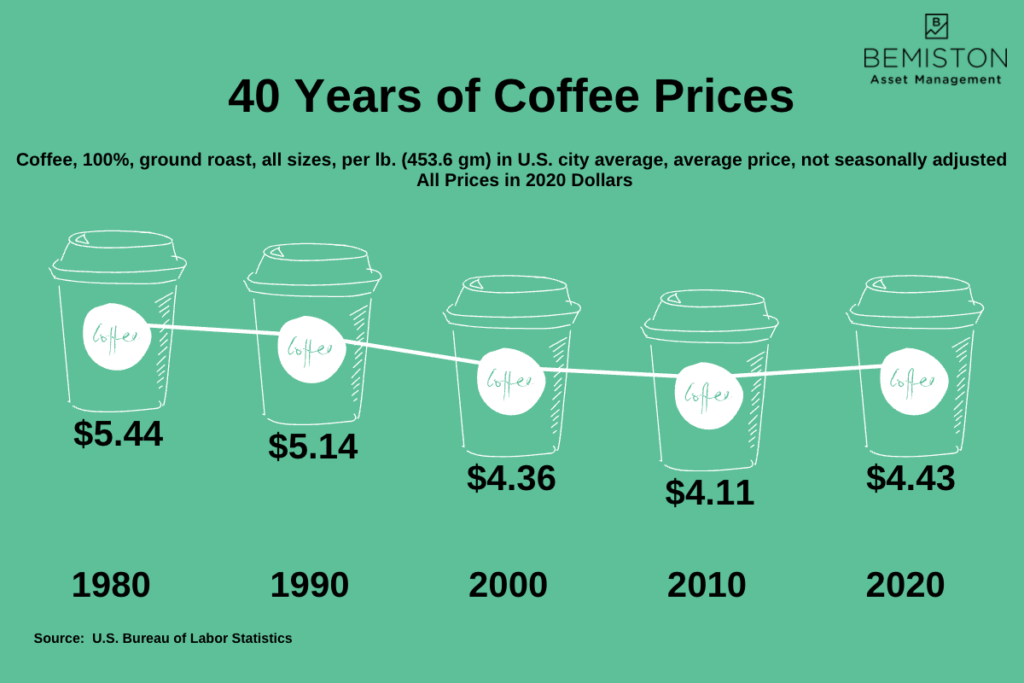

But First, Coffee

Take coffee, for example—just a simple cup of coffee. Not a PSL or caramel macchiato or whatever these are. It takes more dollars now to buy a cup of coffee than it did in the past. A pound of coffee cost $3.14 in 1980, and that same pound of coffee cost $4.43 in 2020. Dollars have lost overall purchasing power. However, when we standardize the price of coffee using 2020 dollar values, we can see that the cost of coffee has risen less than the rate of average consumer inflation. A pound of coffee cost $5.44 in 1980 and $4.33 in 2020.

You Should Have a Financial Advisor If You Can Remember This

Not all price changes are inflationary. Sometimes consumers gain purchasing power on things over time, such as consumer electronics. And that’s not even adjusting for the quality improvement. Remember when the first HDTVs cost at least $8,000? Now you can find HDTVs for a fraction of the cost, and they are so much better. It’s hard to keep track of price changes and quality over time. Still, the BEA and BLS do a pretty good job tackling these challenges for investors and policymakers with the PCE and CPI.

How Does Inflation Work?

Ultimately, inflation results from an increase in the supply of money. Put differently, more money chasing the same amount of goods. Money can be printed and given away by a nation’s treasury, and thereby devaluing it. More commonly, new money creation comes from banks extending credit to businesses and consumers beyond bank reserves. The US Federal Reserve supports and monitors this process. There are three general causes of inflation.

Demand-Pull Inflation

We get demand-pull inflation when the overall money supply increases faster than the economy produces goods or services. More money production as consumers and businesses borrow and spend more quickly than producers can make goods causes inflation. How it works: more dollars chasing the same amount of goods causes inflation. There is a gap between supply and demand, so demand pulls prices higher.

Cost-Push Inflation

Cost-push inflation is when the inputs of a product or service rise in price and then cycle their way through production, causing inflation of the final price. Any supply shock or supply chain disruption can cause the price of intermediate goods to inflate, increasing the cost of intermediate and final goods. How it works: a few minor increases in input prices can spark consumer inflation across a wide variety of goods and services.

Built-In Inflation

Also known as wage-price spiral inflation, built-in inflation results from natural inflation expectations of producers and consumers. People assume a natural, stable level of price increases over time. Because of these expected inflation expectations, workers and producers “bake in” price increases into wage expectations and costs. How it works: higher wages result in higher costs and vice versa, causing inflation. This cycle continues on and on until an outside factor disrupts or we all die.

Winners and Losers

For many, inflation can be insignificantly beneficial and harmful simultaneously, and rapid and unpredictable inflation is terrible for literally everyone.

Winners

Any tangible asset “priced” in a currency can generally benefit from inflation. The asset naturally increases with the money supply: stocks, property, and commodities are a few examples.

Borrowers

Also, debtors that pay a fixed amount and indebted governments come out ahead with inflation. When inflation increases more than expected, those who owe a fixed amount with a predetermined payment will pay less in real terms (inflation-adjusted). Borrowers and lenders have a natural level of inflation baked into the loan, so it’s the extra bit of inflation that matters here.

Also to be noted, firms that can avoid increasing wages at the rate of inflation. How it works: inflation is at 3% and your firm only gives you a 2% raise; you have effectively received a real-wage decrease. It may not seem like much, but it can start to affect living standards over a decade.

Losers

People that stuff their money under the mattress lose out to inflation. Also, people who keep money in bank savings accounts earning sub-inflation level interest lose, too.

Inflation won’t hurt too much if you are saving for general consumption over a short period. However, stashing cash in a saving account for a home purchase over a prolonged period can be an issue. When housing prices are increasing at a rate well over your savings account’s interest rate, you will always slip further and further behind. To meet that goal, you will need to save more for a longer time.

Anyone receiving a fixed income and will not see any cost of living adjustments or pay raises. Many retirees and some fixed-income workers would fall into this category.

Lenders

Lenders that lend on a fixed rate also lose out. If inflation increases faster than anticipated, the interest collected will fall in real terms. It may not seem like a big deal and even beneficial to some. However, suppose lenders are uncertain about the future rate of inflation. In that case, they may be less willing to lend or significantly increase the lending rate. These circumstances would be damaging to economic growth as a whole. High, unpredictable inflation is terrible for everybody.

Small Predictable Inflation Rates Are Good

A little dab’ll do ya. Small, predictable higher prices can be good for the economy. Economists often talk about how higher prices can grease the “economic wheels” or something like that. A little bit of inflation works well when it causes those who hold capital to invest. They know that idle money will naturally lose value. Putting capital to work will grow the economy. Plus, nobody likes a hoarder.

A little inflation can also be good for employers who want to pay less. Rather than giving outright pay decreases, which would cause mutiny, employers can provide pay increases at less than the average inflation rate. Doing this decreases a worker’s real wage.

Price Stability Has Tradeoffs

In the United States, the Federal Reserve Bank promotes a stable financial environment for economic growth, which is much easier said than done. Obviously. The Fed is often said to have a dual mandate of maintaining price stability and maximum(ish) employment.

Dual Mandate

However, these objectives can seemingly conflict. During rapid economic expansions, prices can rise quickly, which may cause the Fed to tap the breaks on the economy and any inflation. The Fed works by controlling the short-term interest rates, increasing the overall cost of borrowing in the economy. Increasing interest rates too rapidly, however, could potentially increase unemployment and even cause a recession. The Fed ultimately tries to maintain a stable price environment that allows businesses and workers to make the best decision about the future, which will lead to full employment.

Quantitative Easing

If you did not hear about Quantitative Easing in the wake of the Global Financial Crisis, you probably heard about it more recently during the Coronavirus Pandemic. Quantitative Easing, or QE, is an aggressive method the Fed uses when times are rough, worse than a “typical recession.” QE entails keeping short-term interest rates near zero and aggressively buying longer-dated maturity bonds in the open market to bring long-term rates down.

Critics suggested that QE would lead to high inflation, if not hyperinflation (over 50%). Hyperinflation never happened after 2008 because consumer and business demand for credit had fallen so much that disinflation was more of a threat. The Fed was essentially trading out cash for bonds to bring interest rates down (Yes, this is a gross simplification).

However, there is evidence that QE fueled housing price increases in metropolitan areas, buoyed the stock of large corporations, and fueled financial risk-taking behaviors.

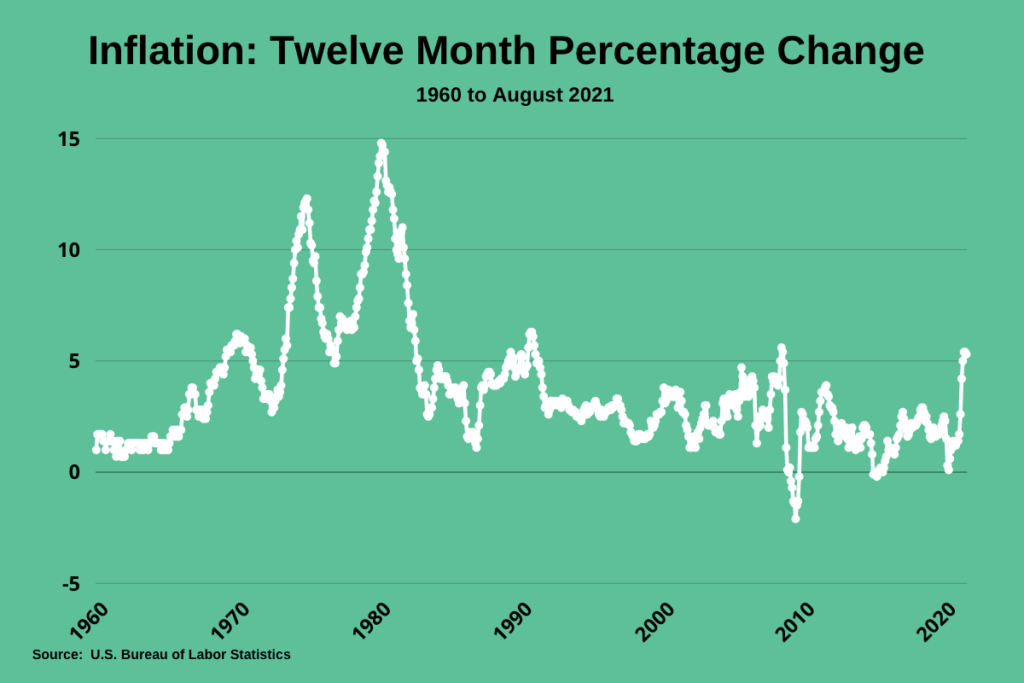

How Fast Are Prices Rising?

As always, the context here is important. Inflation has been ticking higher for the first time in a generation. Some are old enough to remember the double-digit inflation of the 1970s to early 1980s. Many attribute this bout of inflation to the 1970s oil crisis; however, that is incorrect. Nixon and the Fed ran huge deficits and used easy money policy to fuel them, creating an era of rapid inflation. This era resulted from some very short-sighted policies from Nixon to get votes, and he bullied the Fed to do so.

Where Are You Going With This?

In 2021, the most recent inflation rate is “only” at 5.3%. Not “Nixon” high, but it is significantly more than we have seen in recent memory. The Biden administration and Fed are being aggressive with both fiscal and monetary policy at the moment, similar to the Nixon era. However, the critical difference is that the US economy is fragile in 2021 and needs some help. The pandemic caused a deflationary environment, which is why policymakers have responded so aggressively. Nixon was trying to juice the job market to get re-elected, no matter the cost, and put in a Fed loyalist to do so. The two environments are drastically different. Slightly higher inflation can be okay while the labor market is healing—that dual mandate.

What Is Going On Right Now?

Usually, a recipe is involved when you have to scroll this far to get to the point. Sorry, no recipe for you, but some of your ingredients are getting more expensive at the store, and higher prices will be the norm for the foreseeable future.

Supply Chain Struggles

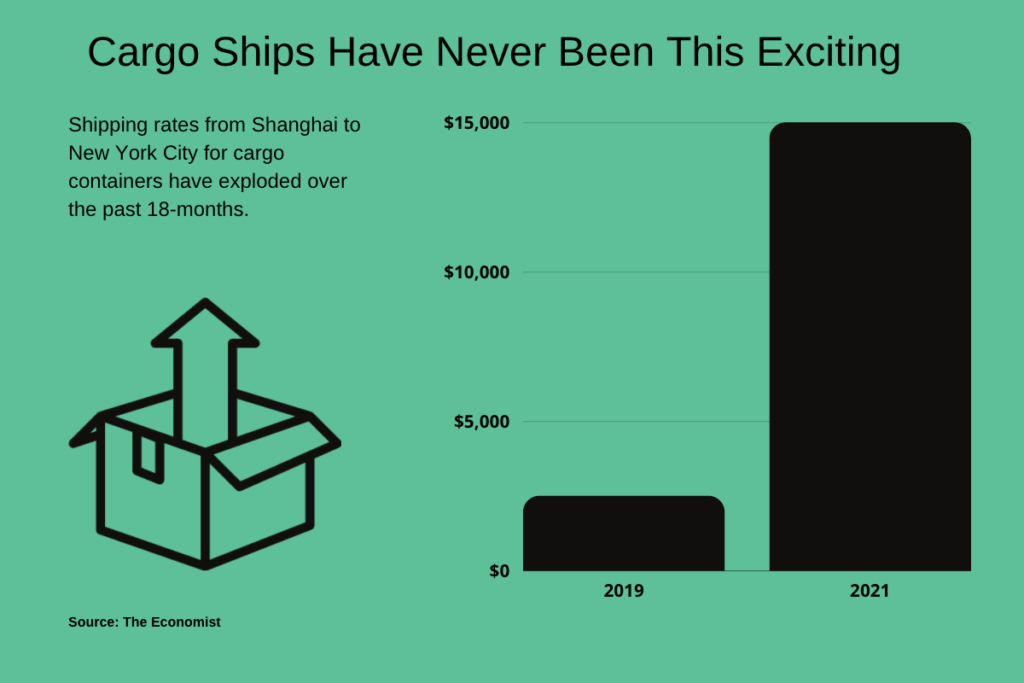

Globally, food prices have been up 32.9% over the past year. Some of the causes are short-term in nature. Supply and shipping bottleneck problems have caused well-noted shortages, particularly shipping containers, as supply chains normalize. Americans are beginning to realize that the world is not reopening at a pace to keep up with a rekindled appetite. There is more demand than there is supply.

Many economies are slower to reopen amid the surge of the delta variant and lackluster vaccine supplies abroad. In some instances, the delta variant has caused ports to close altogether, wreaking havoc on supply chains. These causes of inflation are expected to be transitory and are widely expected (hoped) to ebb by spring. However, if delta or other variants become problems, the price increases could become sticky.

Some Inflation Will Remain

Unfortunately, some of the higher price causes are here to stay for a while. Climate change is causing record-breaking droughts in Brazil, causing coffee prices to soar. Also, China and other developing economies will continue to grow their imports, putting upward pressure on prices. One of the largest grain exporters, Russia, recently imposed an export tax to offset rising prices. These things will have a much stickier impact on inflation than supply chain struggles.

Inflation Cause We Need to Worry About

How will we know inflation is here to stay? Wages. Employers are offering higher hourly wages to lure workers back into the workforce, and some workers have decided not to go back into the service sector. The reasons are highly complicated and not only wage-driven (perhaps another long blog post?). With that in mind, if we begin to see wage increases demanded due to anticipated consumer price increases, we should worry. Then will we the wage-price spiral inflation that is particularly sticky. As of right now, the increase in wages is the result of a demand for workers.

Consumers Expect Higher Inflation Rates

The New York Federal Reserve recently published that consumers expect inflation rates of around 4% over the next three years. But inflation expectations can sometimes be a bogus stat. Supply constraints are part of the problem, but fiscal stimulus in the US has also increased aggregate demand over the short run as economies reopen. These factors may seem contradictory, but hourly wage growth over the next few months should tell us more.

What Will the Fed Do?

The more prolonged inflation persists, the less likely it is to be “transitory” or temporary. The higher that inflation ticks and the longer it goes for will cause the Fed to taper QE and raise interest rates sooner than it would like. Doing so would effectively reverse the support for the economy and the job market when unemployment remains high. What that time frame will be is anybody’s guess. The Fed has very effective tools to choke off inflation, but those tools would stop growth in the process.

How Investments Work With Increasing Inflation Rates

Cash

Not cash. Never cash. Cash is not an investment, especially when a rising inflation rate is your concern. You can hold cash when you are looking to spend it soon(ish).

Stocks

Stocks are generally a good hedge against inflation. Publicly-traded corporations can usually push higher costs off to consumers, and the more expenses they can move off to consumers, the better the hedge. A broad-based index fund or ETF can be an excellent place for investors to use equity-based inflation hedges.

Commodities

Commodities are another classic inflation hedge for investors. A basket of necessary commodities (soybeans, corn, gas, etc.) naturally has its costs flow through to users of that commodity. Investors can easily purchase a commodity ETF or mutual fund that hedges against inflation.

Gold

Let’s talk about gold for a second. I always hear/read about it being a good hedge against inflation. Still, in reality, it has a trash record of doing so. There is no guarantee or evidence that spikes in inflation will result in a proportional increase in gold prices. Gold is a speculative instrument that does not generate economic value. But it is shiny. Unless you are an old prospector, other assets are a better bet against inflation. The same goes for crypto.

Real Estate

Incoming producing real estate is a good hedge versus inflation. Real estate works as inflation rises, real estate owners can increase the rent in proportion to expected price increases. Investors can easily tap into this hedge through a Real Estate Investment Trust or REIT.

TIPS

Treasury inflation-protected securities, or TIPS, are US government bonds that are indexed to inflation and adjusted accordingly. As far as a very safe, pure CPI hedge, TIPS are great, and investors can easily access TIPS via a mutual fund or ETF. The only issue is that TIPS won’t pick up inflation that may occur outside of the CPI.

Conclusion

Inflation is up significantly more now than it has been in my lifetime, but it still remains historically low. While there are some genuine concerns about food prices, many still think these inflation rates are transitory in nature. As the pandemic wanes, supply chains re-establish, and economies normalize, the demand and supply-driven pressures on inflation should abate. Much like this pandemic, it just may continue longer than global consumers and the Fed are hoping.

Learn more about Bemiston Asset Management

If you would like to learn about navigating your portfolio through uncertain times and about how I can help you, you can learn more here.

Sign up for updates

If you enjoy my long-winded, informative, and somewhat entertaining blog posts, please subscribe here to stay updated.