Financial markets are always a little weird. After all, financial markets reflect the behavior and sentiments of people, especially in the near term. Investors have experienced sentiment all over the place the past few years, from bleak circumstances to euphoric speculative nonsense, and back again. 2022 will probably go down as one of the market’s worst years, perhaps even worse than the 2008 meltdown.

Things started fine.

People were optimistic about beginning the year. Sure, the Fed was pulling back on quantitative easing and increasing rates, effectively taking away the punch bowl. However, the labor market is still strong, with low unemployment and many job openings. People can still make the economy go because they have jobs and can spend money.

Many big Wall Street investment firms were betting the Fed could peel back its easy monetary policy, and the economy and market would soar! Here is a look at some predictions from around this time last year for the S&P 500 as gathered by David Armstrong, CFA:

- Barclays – 4,800 (12/2/2021)

- Bank of America, Savita Subramanian – 4,600 (11/23/2021)

- BMO, Brian Belski – 5,300 (11/18/2021)

- BNP Paribas, Greg Boutle – 5,100 (11/22/2021)

- Credit Suisse, Jonathan Golub – 5,000 (08/09/2021)

- DWS, David Bianco – 5,000 (12/1/2021)

- Goldman Sachs, David Kostin – 5,100 (11/16/2021)

- Jefferies, Sean Darby – 5,000 (11/23/2021)

- JPMorgan, Dubravko Lakos-Bujas – 5,050 (11/30/2021)

- Morgan Stanley, Michael Wilson – 4,400 (11/15/2021)

- RBC, Lori Calvasina – 5,050 (11/11/2021)

- UBS, Keith Parker – 4,850 (09/07/2021)

- Wells Fargo – 5,100-5,300 (11/16/2021)

- Yardeni Research, Ed Yardeni – 5,200 (11/28/2021)

Currently, on December 28, 2022, the S&P 500 Index is at 3,800(ish). A far cry from even the more reserved of forecasts.

Short-term forecasts are generally garbage. There will always be an extreme event that drives the narrative over short-term horizons. Over longer horizons, extreme events matter less.

Professionals at big firms got it very wrong. They assumed inflation would run off faster than it did. A classically difficult to predict factor, geopolitics also proved to be a big story earlier in the year.

It’s all about the Fed

So what went wrong? What’s the narrative driving 2022? Well, a few things went wrong.

- War in Ukraine

- Inflation went higher

- China remains closed(ish)

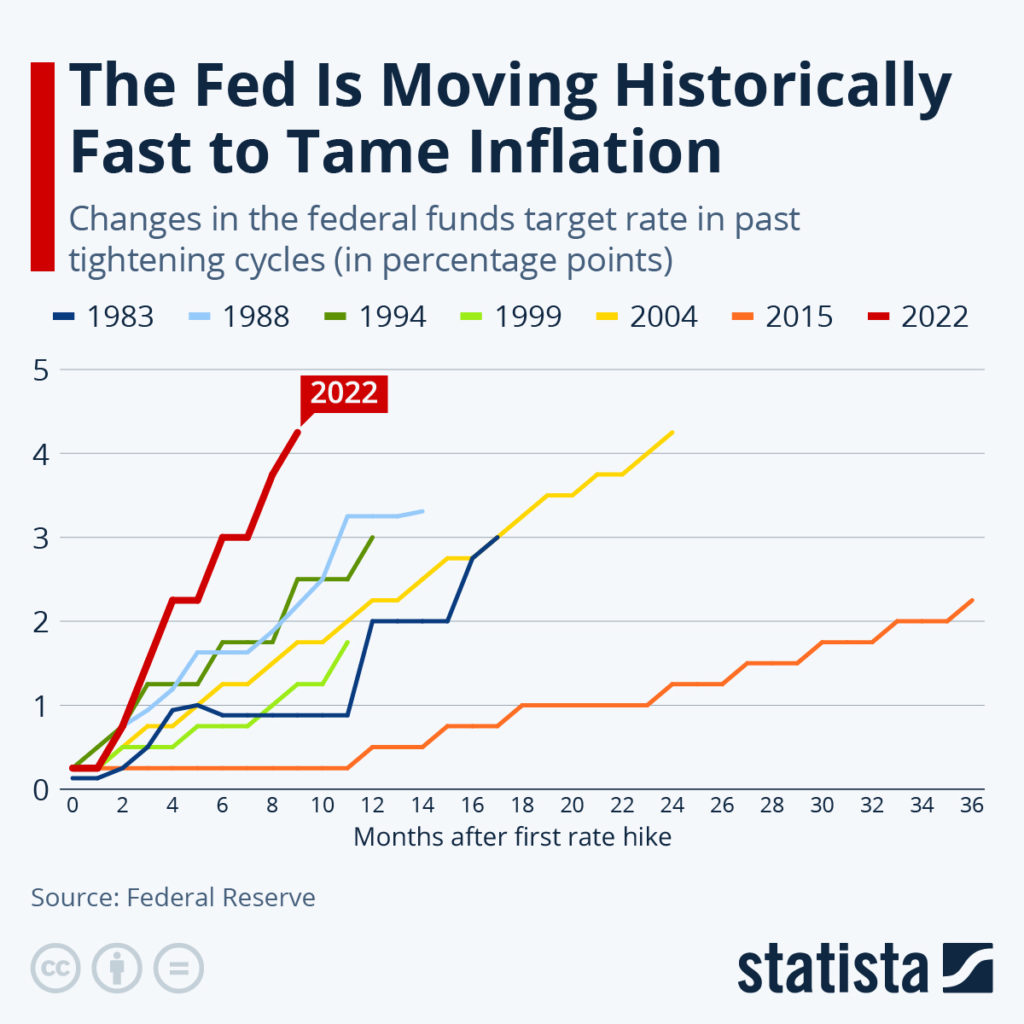

- The Fed increased rates from 0.25% a year ago to 4.50% today

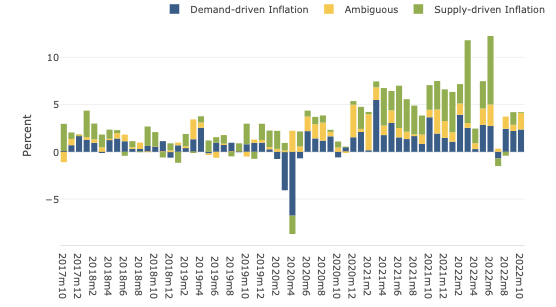

The war in Ukraine and Chinese policies have added to the supply-side woes affecting inflation. Things the Fed has no control over. The Fed does have some influence on the demand side, but its toolset is not ideal.

This graph from the Federal Reserve shows the breakdown of these causal components. Rate hikes can only really affect the blue bars. Hikes may make the green bars worse off in the long run.

The Fed feels like the only way it can bring inflation down is to get wage growth down. Wage growth is over 5.00%(ish). If wage growth remains high, there will be continued inflationary pressure.

To bring wage growth down, the Fed is raising rates quickly. Higher rates will lower the demand for new workers, cool the economy, and increase unemployment, which will cool inflation. The Fed is essentially trying to kill demand by creating a recession (even a mini one).

Investors have had a terrible year.

The Fed is nuking the economy to bring inflation back in line. So, while the inflationary pressures ebb, the fears of recession loom. The recessionary concerns, in conjunction with rapid interest rate increases, have crushed investors this year.

| Index | Return |

| S&P 500 | -20.7% |

| NASDAQ | -34.31% |

| Bloomberg’s Bond | -12.97% |

| Bloomberg US Treasury | -12.85% |

The classic portfolio of 60% stock and 40% bonds has had its worst year in a century. The portfolio is supposed to hedge against both assets falling simultaneously. It did not work. A 60/40 portfolio is off about 17% this year.

Economic uncertainty leads to a stock selloff. Increasing interest rates lead to a selloff in bonds. There has been a shift in the stock market from technology-heavy growth stocks to cash-generating value stocks.

Investing in 2023

Higher interest rates and economic headwinds have shifted investor focus from narrative-heavy stories of disruption to cash-flow-producing financial stalwarts. Investors are less concerned about promises of enormous profits in the distant future. In a challenging environment, investors want a return on investment sooner rather than later.

The economic regime is changing. The era. of ultra-low interest rates seen after the Global Financial Crisis is coming to an end. Investors should not expect it to return. As the cost of capital increases, investors need to look beyond technology stocks and the S&P 500 for returns.