One of the most common questions a financial advisor gets is paying off debt vs. investing. More specifically, is it better to pay down debt or invest? Should you delay retirement savings to pay down a mortgage or student loans? Should you pay off debt before starting an emergency fund?

The simple answer is that you should be doing all three things: investing for retirement, building savings for an emergency, and paying down debt. The tricky part is juggling all three things efficiently to meet your financial goals according to your unique values.

Various factors figure into your decisions on prioritizing your cash to meet your needs.

The Interest Rate of Debt

One of the essential factors in figuring out your priorities is the interest rate of your debt. High-interest rates are a killer. Credit cards can carry interest rates in the high teens to upwards of 20%.

There is no way to earn a reliable rate of return that is over the interest rate you pay in credit card debt. You can’t clear that 20% interest hurdle by investing. The only way to get out of credit card debt is to pay it down.

Is It Better to Pay Off Student Loans or Invest?

A good financial advisor would never recommend complete austerity until your debts are wiped clean. You need to live your life. However, there is a fundamental economic tradeoff between debt repayment, consumption, and investing. That tradeoff becomes a little more complex as the costs of debt decrease.

Lower interest rates in the mid-single digits, such as student loans or mortgages, are far more manageable than credit cards. Around 90% of federal student loans have interest rates between 3.73% and 6.28%. Once a student loan borrower has met their monthly minimum payment, should they pay that debt down? It depends.

For example, student loan debt of around 5% is a relatively easy burden to carry. Suppose the borrower is willing to invest in the stock market, historically earning around a 10% annual return. Making a spread of 5% is enormous, and it snowballs your savings over time.

Is It Better to Pay Off a Mortgage or Invest?

Is it better to pay off a mortgage early or invest? We can also apply the same investment versus debt interest rate framework here. Nationally, average mortgage rates are around 3-4%, which is a relatively low hurdle to clear within your typical investable universe of stocks, bonds, real estate, etc.

Mortgages are also a little trickier because of amortization. Most of your early payments go towards the loan’s interest, even though your monthly payment is the same. So, you build the majority of the equity in your home towards the end of the mortgage.

If you want to pay off your mortgage early, you would want to make larger payments earlier. The majority of your mortgage payments at the end go toward the equity in your home. If you pay more on your mortgage towards the end of the loan, you are essentially just paying yourself with your own money.

Mortgage vs. Investing: An Example

Even with this mortgage amortization stuff in mind, investing over paying down your mortgage early makes more sense. Investing earlier allows you to compound your savings much faster than earlier mortgage repayment. Let’s look at an example:

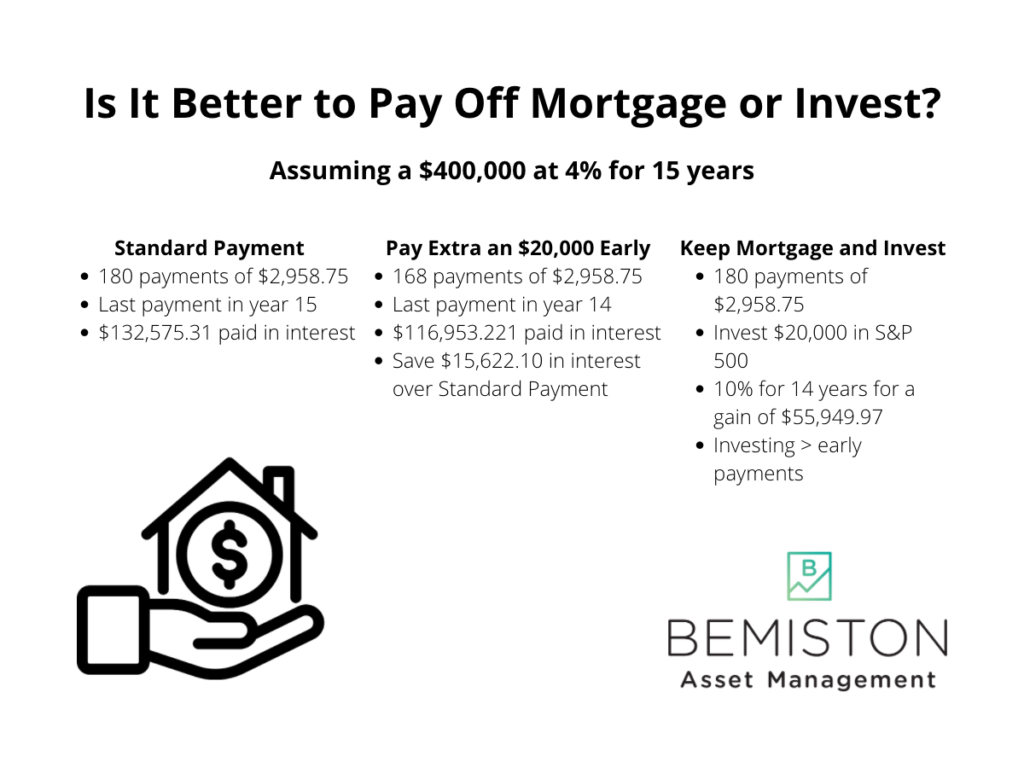

Let’s assume a $400,000 mortgage loan at a fixed rate of 4.00% for 15 years. We will ignore taxes and homeowners’ insurance to keep it simple. It won’t change the conclusion.

In this scenario, the payments are $2,598.75 a month. Of the first payment, $1,625.42 will go towards the principal, and $1,333.33 will go towards the interest portion of the mortgage. The final payment will occur in year 15 (payment number 180) with $2,948.92 towards principal and $9.83 towards interest. Amortization!

If, on the first payment, you decide to throw in another $20,000, it will all go towards paying down the principal of the loan. You have effectively reduced the outstanding principal by $20,000. The last payment will occur an entire year earlier by paying down extra early in the mortgage, saving over $15,000 in interest payments. Sounds great, right? Maybe not.

What if you did something else with that $20,000 instead? Let’s say you invested $20,000 in the S&P 500 Index over 14 years (from the early payoff example). Over the past 30 years, the index averaged 10.72%, so we will say 10% to keep it simple. Investing $20,000 at a 10% return for 14 years results in a gain of $55,949.97. Over $40,000 more than the interest savings from early mortgage repayment!

There Are Other Reasons to Pay Off Debt

Being debt-free is an admirable goal, but it may not be the most financially savvy one. However, there are other reasons to take a step to lower your debt.

As mentioned previously, carrying credit card debt or other high-yielding debt can be a natural killer, and you should pay that off ASAP. Credit card debt can hover around 20%, and there is no reliable way to earn that rate consistently in the market.

Your credit utilization ratio is how much credit you are using compared to how much you have available. Having a high credit utilization rate can affect your credit score. A poor credit score can limit your ability to rent, receive favorable interest rates, or even get a loan. Maintaining an appropriate level of debt is essential to your financial goals.

Ideally, you allocate your resources to build an emergency fund, invest for your future, and pay off debt. All three things are critical for your financial security and success.

You Need to Be Investing

Generally speaking, you will earn more from compounding interest than the early pay down on debt. While all debt is not the same, mortgage and student loan debt is typically around 5%, give or take.

Investing in a diversified stock mutual fund can earn you about 10% annually. This difference will stack up over time. The more you invest rather than pay down will leave you much better off.

How to Invest

Firstly, be sure that you meet your employer’s 401(k) match, as it’s free money. Saving for retirement is crucial as you cannot take out a loan to retire. Start early and let the power of compounding work for you. Using a retirement account for investing is the most tax-efficient way to grow your investments.

Secondly, see if you can invest in a Roth IRA if you qualify. A Roth IRA allows you to invest your current savings and withdraw them tax-free in retirement. Another advantage of the Roth IRA is that you can always take out your contributions if you need them in an emergency.

Read More: When Roth IRAs Make Sense for Millennials

After that, you can invest in a regular old taxable brokerage account. You can still invest tax-efficiently, but any selling you do is subject to your prevailing capital gains tax rate.

Perhaps You Really Want to Pay Down Debt

It might not be technically correct, but if having debt keeps you up at night, maybe you should pay it off. If your debt interest rate is relatively high, paying off it first might make sense. Especially credit card debt, as the average interest rate can be close to 20%.

Carrying mortgage or student loan debt is a lot less strenuous than credit card debt. It can be easy to meet the minimum payments and continue to invest. However, if you want to prioritize debt repayment first, that is fine. Start by paying off the highest interest rate debt first, then move on to the next highest rate.

It could also make sense to prioritize debt when utilizing more than 25% of your credit. By paying off some of your debt, you can improve your overall credit score for the next time you wish to apply for a loan, apartment, or a job that requires a credit check.

Being able to pay off or pay down your mortgage or student loans is a great thing. Paying off your loans is an integral part of financial wellness, just as much as saving for retirement.

Using a financial advisor can help you figure out how to balance student loan payments, extra payments for your mortgage, and saving retirement.

Read More: A Financial Wellness Guide for Millennials